Code Green Solutions

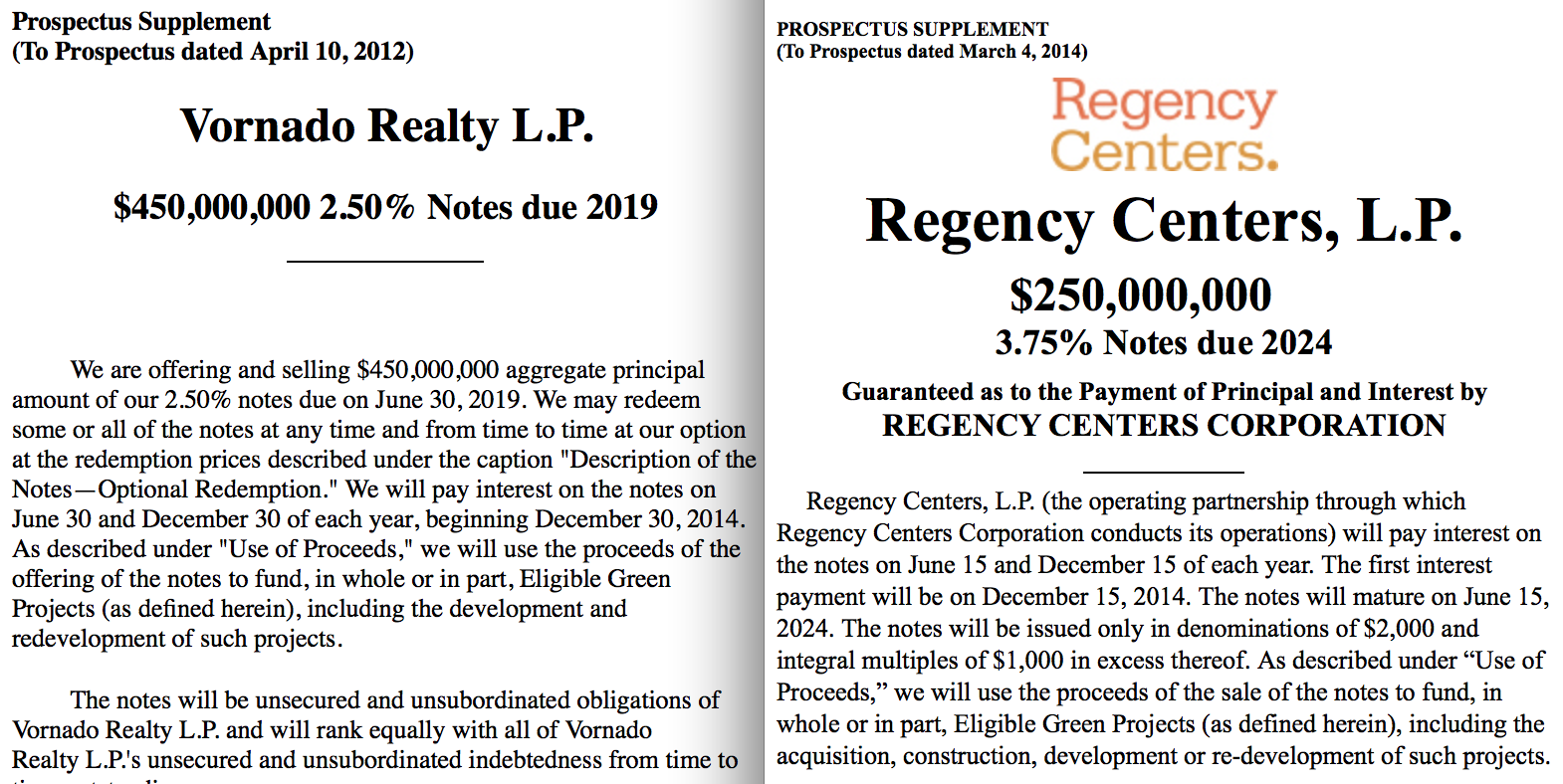

In the second quarter of 2014, two major publicly-traded commercial real estate investment trusts raised a combined $700 million in general obligation debt for investing in real estate development and/or retrofit projects identified as ‘green’.

These bond offerings — $250 million by Regency Centers and $450 million by Vornado Realty Trust — were sold by a syndicate of global investment banks and marketed to investors as ‘Green Bonds’. Investment banks and their REIT clients correctly identified the significant pent-up appetite for Green Bonds, and successfully crafted debt offerings to tap this market segment. Demand was strong led by the $13.6 trillion socially responsible investment community, with traditional bond investors already familiar with each company’s risk profile jumping in as well.

As an emerging financial product, Green Bonds create new disclosure requirements to adequately define ‘green’ while also serving to broaden a company’s investor appeal in an ever-evolving capital market landscape. Investors implementing risk reduction strategies or seeking add-on benefits with their investment activities are advised to request additional detailed information on corporate track records with green real estate investment and operations, perform deeper assessments into green claims, and refine investment criteria to better align expectations.

Certifying property holdings to the LEED green building rating system is a necessary component to underwriting and validating a Green Bond from an asset level perspective. At the corporate level, understanding a company’s overall sustainability performance [GRESB, Global Reporting Initiative, Carbon Disclosure Project] will serve to further differentiate opportunity and risk in the eyes of investors.

This GBIG Insight White Paper Green Bonds: REITs Find Strong Demand For High Performance Property Financing [see PDF] provides the background context necessary to understand:

1) what does ‘Green Bond’ mean in the real estate capital market environment

2) how does a Green Bond label shape investor expectations

3) what additional disclosures investors should require when underwriting the next wave of Green Bonds

Over the near term, greater transparency and disclosure on specific aspects of a company’s track record with green building is required to properly determine an investment risk profile. Green Bond investors should anticipate a fast-paced market evolution as real estate companies work hard at one-upping their peers in the pursuit of investment dollars at favorable rates.

{kind=link}